The Role of AML and KYC in Modern Fintech: Chimoney’s Approach to Compliance

Introduction

The rise of digital finance has revolutionized global payments, enabling seamless transactions across borders. However, this rapid growth has also introduced new risks such as money laundering, fraud, and financial crimes that regulators seek to mitigate. Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations are at the core of financial compliance, ensuring that fintech companies operate securely while preventing illicit activities.

At Chimoney, compliance is embedded in our operations. As we expand our footprint globally, including in Canada, we remain committed to maintaining robust AML and KYC frameworks that align with Canadian regulatory standards under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) and oversight by the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC).

Understanding AML and KYC in the Canadian Fintech Ecosystem

What is Anti-Money Laundering (AML)?

AML regulations are designed to prevent financial institutions and payment companies from being used to launder illicit funds or finance criminal activities. These laws require fintech companies like Chimoney to:

- Monitor and report suspicious transactions.

- Conduct due diligence on customers and businesses.

- Implement strong internal controls to prevent money laundering.

In Canada, AML laws are primarily enforced under the PCMLTFA, with oversight from FINTRAC.

What is Know Your Customer (KYC)?

KYC is a subset of AML that requires financial institutions to verify customer identities before they can access financial services. This ensures that fintechs like Chimoney:

- Verify users' identities using government-issued documents.

- Assess the risk level of customers and monitor transactions.

- Prevent fraud by ensuring only legitimate individuals and businesses access financial services.

Under Canada’s AML regime, KYC is mandatory for businesses engaging in financial transactions, including those categorized as Money Services Businesses (MSBs).

Key AML & KYC Regulations in Canada

1. The Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA)

The PCMLTFA is Canada’s primary AML law, requiring fintechs like Chimoney to:

- Register with FINTRAC as a Money Services Business (MSB).

- Conduct customer due diligence (CDD) to verify customer identities.

- Monitor and report suspicious transactions that could be linked to money laundering.

- Implement record-keeping requirements for transactions over CAD $10,000.

2. FINTRAC (Financial Transactions and Reports Analysis Centre of Canada)

As Canada’s financial intelligence unit, FINTRAC oversees AML compliance and requires fintech companies to:

- Submit Suspicious Transaction Reports (STRs) when identifying potential money laundering activities.

- Submit Large Cash Transaction Reports (LCTRs) for transactions over CAD $10,000.

- Develop AML compliance programs, including employee training and internal risk assessments.

3. The Retail Payment Activities Act (RPAA) and AML Compliance

Under the Retail Payment Activities Act (RPAA), which Chimoney has completed registration for, specifies that payment service providers must meet AML/KYC obligations similar to those of banks, ensuring all users and transactions comply with Canada’s financial security standards.

How Chimoney Ensures AML & KYC Compliance in Canada

At Chimoney, we have implemented a comprehensive AML & KYC framework to comply with FINTRAC and RPAA requirements while providing a secure and seamless payment experience.

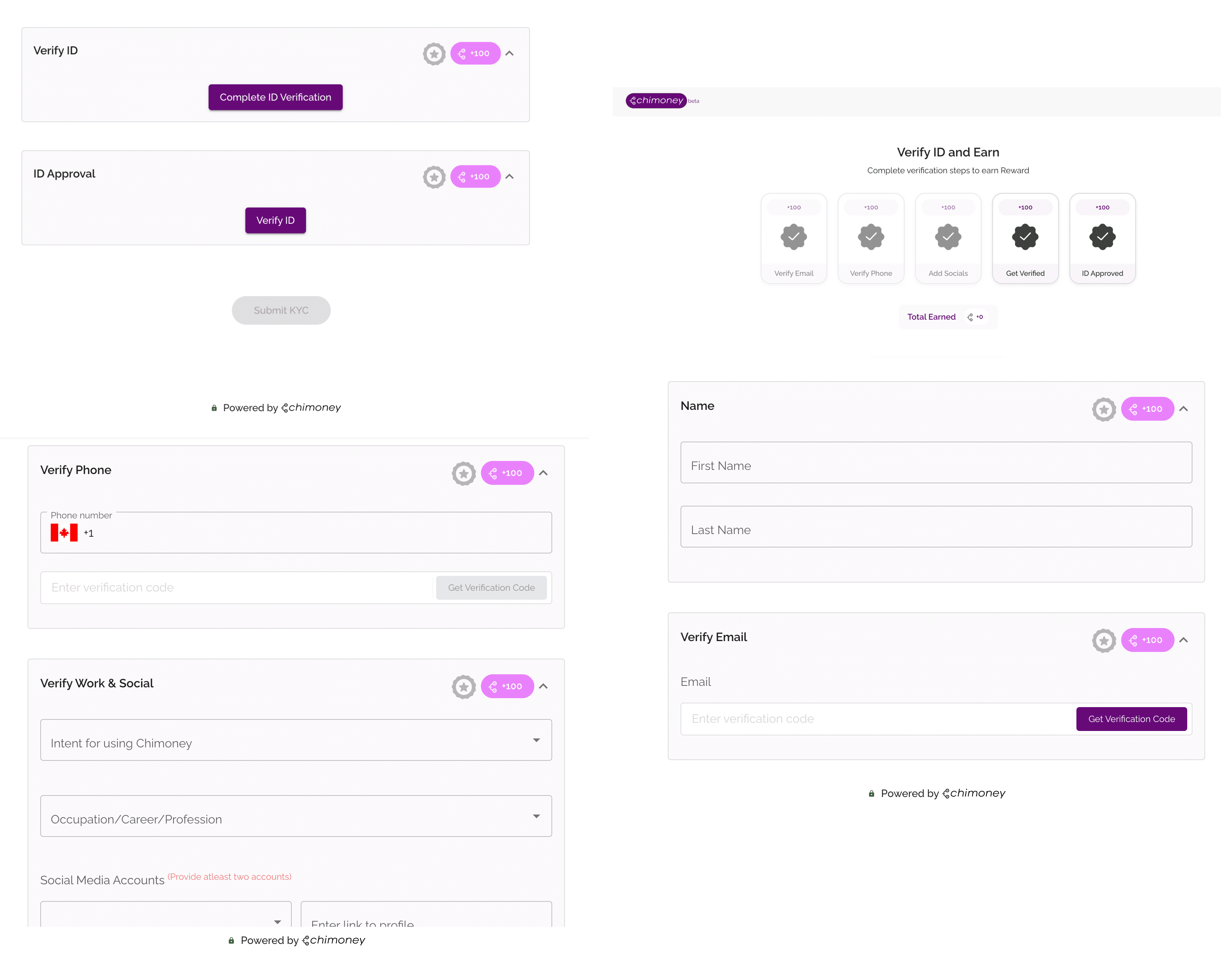

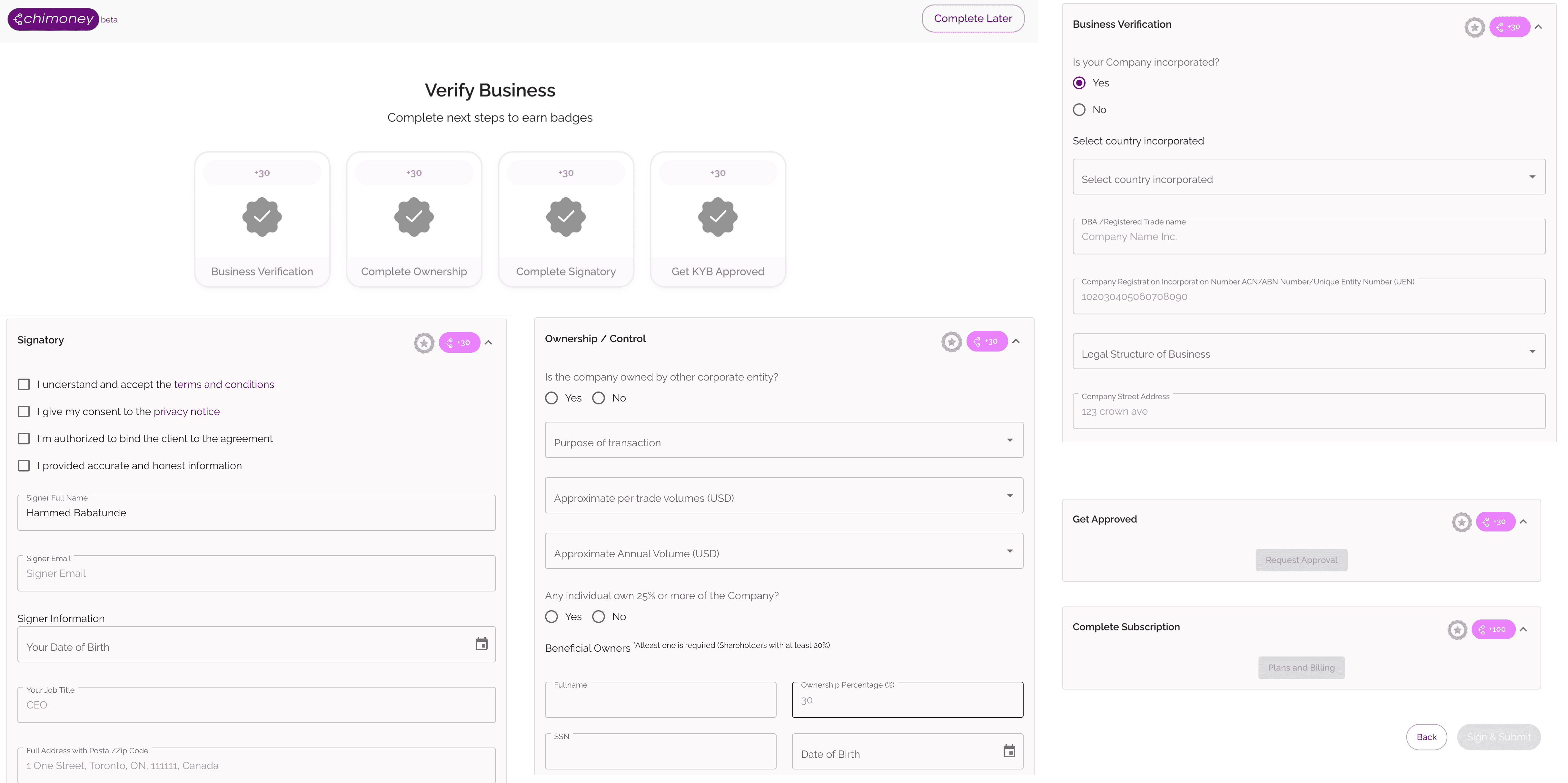

1. Customer Verification and KYC Procedures

-

Identity Verification: We require customers to submit valid government-issued IDs (e.g., Canadian passports, driver’s licenses).

-

Automated Document Checks: Our system cross-verifies ID documents using the automated KYC technology.

-

Address Verification: Users may need to submit proof of address (utility bill, bank statement) for additional security.

-

Enhanced Due Diligence (EDD): High-risk users undergo deeper background checks before account approval.

2. Transaction Monitoring & Fraud Detection

- Risk Assessment: Our system analyzes transactions in real time to detect unusual patterns.

- Suspicious Activity Reporting: We report flagged transactions to FINTRAC as required by Canadian law.

- Geofencing & IP Monitoring: We block high-risk jurisdictions from accessing our platform.

- Blacklist & Watchlist Screening: We screen users against global sanctions lists (OFAC, Interpol, etc.).

3. Secure Business and Merchant Onboarding

Business KYB (Know Your Business): All corporate clients must provide:

- Business registration details.

- Beneficial ownership information.

- Proof of compliance with AML/KYC regulations: Each merchant is assigned a risk level based on industry, location, and transaction volume.

We continuously review our merchant accounts to ensure compliance.

The Future of AML & KYC Compliance in Canadian Fintech

Regulations are evolving, and Chimoney is proactively adapting to ensure full compliance. Some trends shaping the future of AML & KYC in Canada include:

- Open Banking Regulations: Expected to bring stricter data-sharing and fraud prevention standards.

- Real-Time Transaction Monitoring: Regulators may require fintechs to enhance AI-driven fraud detection.

- Increased Cross-Border Scrutiny: With globalization, AML enforcement agencies are focusing on multi-country compliance frameworks.

Chimoney is at the forefront of these changes, ensuring that we remain compliant while delivering seamless global payouts and collections.

Conclusion

AML and KYC compliance are non-negotiable for fintechs operating in Canada. With growing regulations under PCMLTFA, FINTRAC, and RPAA, Chimoney is committed to staying ahead by implementing cutting-edge compliance technologies and ensuring that all transactions are secure, compliant, and fraud-free.

At Chimoney, compliance is more than just a requirement. It’s our promise to users, businesses, and regulators. By adhering to Canada’s AML & KYC regulations, we continue to build a trusted, secure, and compliant payment ecosystem for all.

Stay updated with Chimoney’s compliance journey by following our blog and LinkedIn updates!

Check out these other posts

Why 2025 Is The Year AI Agents Get Their Own Wallets (And Passports)